I promise this blog isn’t solely about Brexit – I think everyone has seen enough of those – but Brexit does play a part.

Brexit has, for funds and managers across the UK, brought attention to the disparity in margin levels calculated by different CCPs. It has therefore unearthed the need to monitor – and regularly shift – where business is cleared.

Why are margins not the same if they are covering the same amount of risk?

In theory, the same amount of risk should be shouldered by the same amount of margin, even across different CCPs. They have, after all, been developed to meet the same or similar regulation.

For OTC, means margin needs to:

- Be based on a 5 day holding period.

- Not be lower than calculations using volatility over a 10 year historical lookback period.

- Cover a confidence level of at least 99%.

- Include components to cover concentration and liquidity risk.

In addition, CCPs all base their algorithms on the same Filtered Historical VaR methodology.

With this in mind, it’s alarming how different margin charges can be.

There are a number of factors that can explain these differences:

- Each CCP has their own methodology used for creating base curves.

- Stress periods need to be included in the margin to avoid procyclicality, and each may select different scenarios.

- For liquidity, CCPs generally consider the cost of hedging the portfolio, but each will have their own view on market spreads and capacity.

So what does this mean in practice?

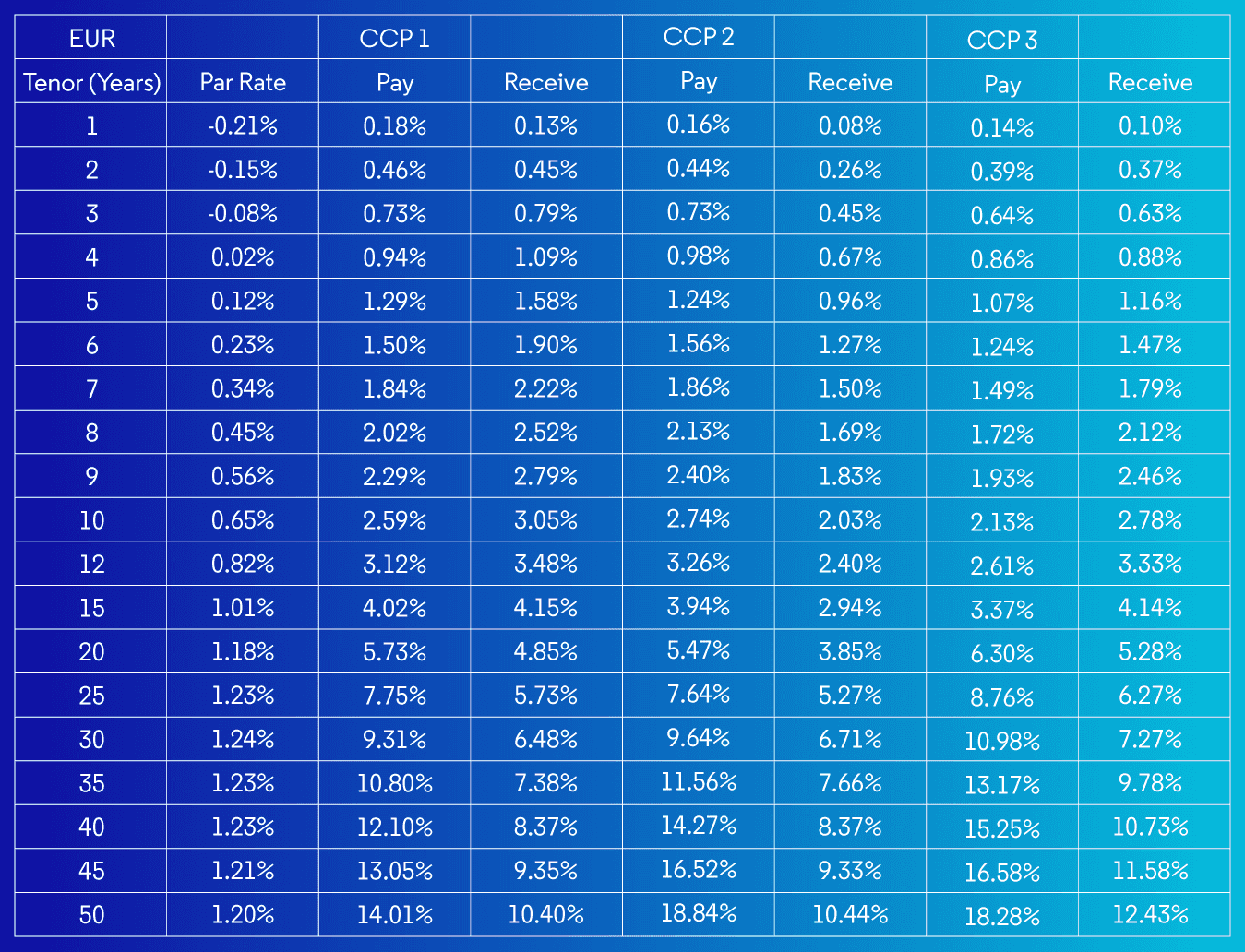

The following table shows, in percentages, example margins calculated on a series of par swaps at 3 different CCPs.

This is on a EUR 1 million notional swap, so would not include liquidity and concentration add-ons.

Our findings

Where CCPs stand in relation to one another is dependent on the tenor of the swap. For example, CCP 3 margin is less than CCP 2 for a 2 year swap, but more than CCP 2 for a 20 year swap.

And looking specifically at the margins calculated, a EUR 100 million notional 20 year swap could mean a saving of over EUR 14 million through CCP 2 rather than CCP 3.

Obviously it’s not quite so simple in real life scenarios. Margin is calculated at portfolio level, so the actual margin that you pay will be dependent on all of your trades; where is cheapest to clear a new trade will be dependent on your existing positions too.

It’s also important to bear in mind that the above table is just a snapshot, and that the values will change over time. While margin charges may be highest at one particular CCP this month, next it could be an entirely different CCP taking that position. From the analysis that we have done, there is no consistent ranking, no same CCP staying higher or lower.

To sum up

The only way to ensure you are choosing the best clearing venue then is to calculate what-if margins for each CCP. Comparing their margin costs with a view to trading through those with the lowest requirements frees up previously tied capital, maximising your returns.

It’s only then that you could save yourself millions in margin reductions.

OpenGamma’s software processes millions of calculations every day, built on years’ worth of trade data, allowing us to create realistic projections for funds and managers to make material savings.